On January 30, 2026, Anthropic released 11 open-source plugins for Claude Cowork — its agentic AI assistant for non-technical professionals. One of them was a legal plugin that automates contract review, NDA triage, and compliance workflows. Within days, investors had erased $285 billion from software, legal tech, and financial services stocks. Analysts at Jefferies gave it a name: the SaaSpocalypse.

Thomson Reuters dropped 16%. LexisNexis parent RELX fell 15%. LegalZoom lost nearly 20%. Salesforce, Adobe, and ServiceNow each declined roughly 7%. Indian IT outsourcers — Infosys, TCS, Wipro — shed 4–6% as markets realized agentic AI directly threatens their billing models.

Here's what's remarkable: the legal plugin that spooked the market is, as Shelly Palmer pointed out, essentially a set of prompts and workflow configurations — not a proprietary legal reasoning engine. Anthropic didn't need a breakthrough product. It just needed to demonstrate what a $100/month Claude subscription could do to workflows that SaaS companies charge thousands for.

This wasn't a one-day panic. It was the market recognizing a structural shift that has been building for years. And there's a powerful framework — decades old — that explains exactly what's happening and where it leads.

The Double Helix of Industry Evolution

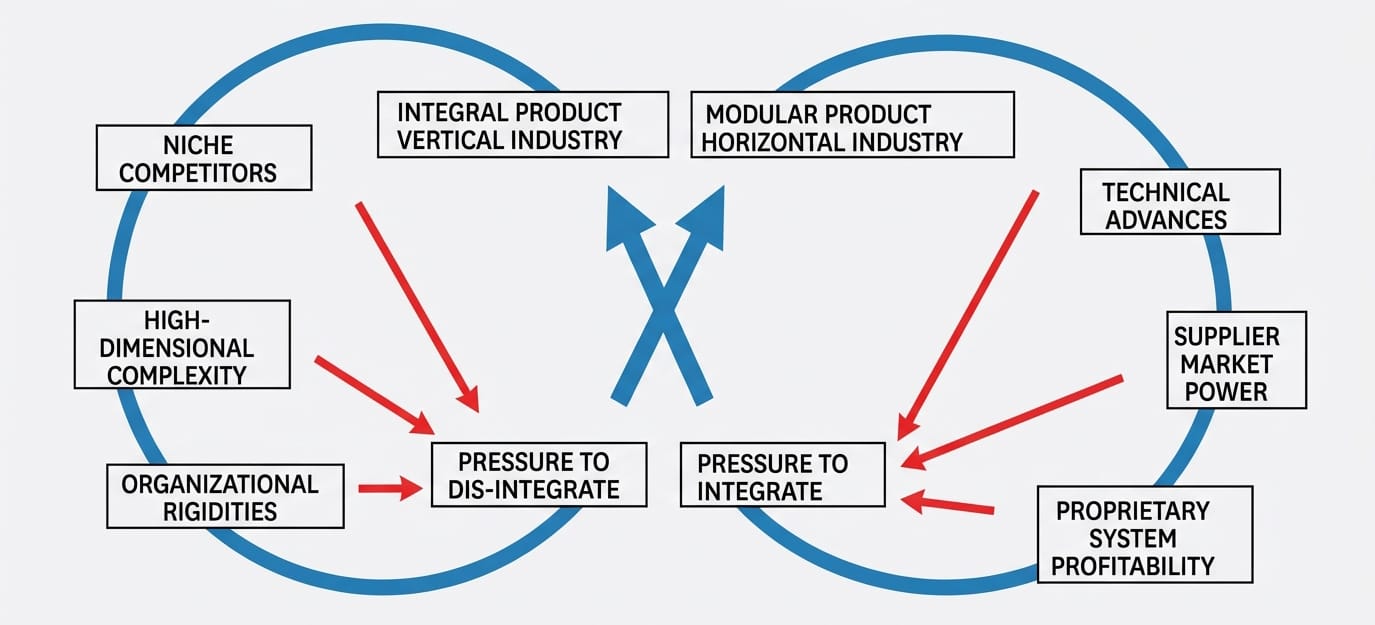

In 1998, MIT professor Charles Fine published Clockspeed: Winning Industry Control in the Age of Temporary Advantage. His central insight was deceptively simple: no industry structure is permanent. Every industry oscillates in a continuous cycle between two states — vertical integration and horizontal modularity — driven by predictable forces. He called this the double helix.

In the vertical/integral phase, a dominant company designs and controls the entire product — from components to customer experience. Think IBM in the mainframe era, Apple with the iPhone, or SAP with enterprise resource planning. These integrated architectures win when tight coupling between components delivers performance, reliability, or user experience that no assembly of parts can match.

But success breeds vulnerability. Three forces inevitably create pressure to dis-integrate:

- Niche competitors target the most profitable slices of the integrated product, often innovating faster or offering lower costs.

- High-dimensional complexity makes the integrated system increasingly difficult and expensive to manage, extend, and evolve.

- Organizational rigidities slow the integrated company's ability to respond, while nimble modular players move at a different clockspeed entirely.

When these pressures peak, the industry fragments into a horizontal/modular phase — specialized companies owning distinct layers of a stack, with open interfaces between them. The PC revolution is the textbook case: IBM's vertically integrated mainframe business gave way to a modular ecosystem where Intel made chips, Microsoft made operating systems, and Dell assembled hardware — each dominating a horizontal layer.

But the helix doesn't stop there. Once the modular phase matures, new forces push toward re-integration: component suppliers accumulate outsized market power, technical advances reward tight coupling, and the pursuit of proprietary profitability drives ambitious companies to re-bundle the stack. And so the cycle continues.

The SaaSpocalypse Is the Helix Turning

Enterprise software has been living in the vertical/integral phase for two decades. Salesforce doesn't just manage contacts — it owns the entire CRM workflow from lead capture through analytics. SAP integrates procurement, manufacturing, HR, and finance into a single ERP stack. Thomson Reuters bundles legal research, case law, AI-assisted analysis, and practice management into one proprietary system called Westlaw.

These are classic integrated smokestacks. And all three disintegration forces are now firing simultaneously.

Niche competitors have arrived — and they're AI-native. Claude Cowork's legal plugin is a focused attacker picking off the highest-value workflow from Thomson Reuters' CoCounsel. It doesn't replicate Westlaw. It targets the specific task — contract review, NDA triage — where 80% of user needs can be met by a general-purpose language model plus structured prompts. The same pattern applies across every vertical: a finance plugin challenges Intuit, a sales plugin challenges Salesforce, a support plugin challenges ServiceNow. Because these plugins are open-source on GitHub, they enable a swarm of further niche competitors to customize and extend them for specific industries.

Complexity has become a liability. SAP implementations routinely take years and cost millions. Salesforce environments sprawl across hundreds of custom objects, workflows, and integrations. This complexity was once a competitive moat — "nobody rips out SAP." Today, it's a vulnerability. A Claude plugin that reviews a contract in seconds doesn't need to replicate the 95% of Westlaw that most users never touch. The double helix predicted exactly this: the integrated system's own complexity becomes the force that breaks it apart.

Organizational rigidities are real. Anthropic's velocity tells the story. Claude Code hit $1 billion in annualized revenue within six months of launch. Cowork launched on January 12; the 11 open-source plugins dropped 18 days later. Enterprise software companies typically spend quarters releasing comparable features. The incumbents' organizational structure — large sales teams, implementation consultants, quarterly release cycles, complex partner ecosystems — makes them structurally unable to match the clockspeed of AI-native companies.

The Emerging Modular Stack

What's forming in place of the SaaS smokestacks is a classic horizontal, modular architecture:

| Layer | Role | Examples |

|---|---|---|

| Foundation Models | General-purpose reasoning | Claude, GPT, Gemini |

| Agentic Orchestration | Coordination of tools, models, data | AnyQuest |

| Vertical Plugins | Domain-specific workflows | Legal, CRM, Finance, Support |

| Data Connectors | Integration with enterprise systems | APIs, MCP, file access |

| Enterprise Data | Proprietary organizational knowledge | Documents, databases, processes |

No single company needs to own the entire stack. A law firm can use Claude as the reasoning engine, a legal plugin for contract workflows, and its own document repository — assembling best-of-breed components rather than buying a monolithic vertical solution.

But here's the critical question the double helix raises: who makes modularity work for the enterprise?

A collection of plugins, models, and data sources is not a solution. It's a parts bin. Someone has to orchestrate it — coordinate the models, enforce security and compliance, route data correctly, maintain audit trails, and ensure the assembled stack actually delivers reliable business outcomes. In the PC revolution, the operating system played this role. In the agentic AI revolution, the orchestration platform plays it.

AnyQuest: The Orchestration Layer for the Disintegration Phase

This is the problem AnyQuest was built to solve. AnyQuest is a collaborative AI platform that brings together models, tools, and data sources into a unified, enterprise-grade orchestration layer — giving organizations the ability to adopt agentic AI while maintaining the security, privacy, and control that enterprises require.

Model independence protects against re-integration risk. The double helix warns that supplier market power will concentrate among a few foundation model providers — just as Intel and Microsoft dominated the PC era's horizontal layers. Enterprises that lock into a single model provider today risk replacing one form of vendor dependence with another. AnyQuest's model-agnostic architecture lets enterprises use Claude, GPT, Gemini, or open-source models interchangeably — hedging against the re-integration pressure the double helix predicts is coming.

Enterprise-grade governance fills the trust gap. Anthropic's open-source legal plugin proved that AI can do the work cheaply. But enterprises still need compliance, data residency, access controls, and audit trails. The orchestration layer is where those controls are enforced. AnyQuest is designed from the ground up for enterprise security and privacy — the critical capability that distinguishes a production-ready platform from a consumer chatbot experiment.

Workflow intelligence compounds over time. Pure model abstraction is a thin, commoditizable layer. AnyQuest goes beyond swapping models — it encodes enterprise workflow intelligence: how approvals chain together, how data governance policies are enforced, how industry-specific orchestration patterns work. Every enterprise that adopts AnyQuest deepens this knowledge, building a compounding advantage that cannot be replicated by a model provider publishing a GitHub repository of prompts.

The plugin ecosystem creates network effects. As vertical AI plugins proliferate — for legal, finance, HR, sales, marketing, customer support — the platform that curates, connects, and manages them gains increasing returns to scale. Every new plugin makes AnyQuest more valuable. Every enterprise customer attracts more plugin developers. This is the same network-effect dynamic that powered Windows during the PC disintegration phase.

The Strategic Window Is Open — But It Won't Stay Open Forever

The double helix is a loop, not a line. The disintegration phase that the SaaSpocalypse has announced will eventually give way to re-integration. New vertically integrated AI platforms will emerge — likely built around whichever orchestration layer has accumulated the most enterprise trust, workflow intelligence, and ecosystem gravity.

The question for enterprises is not whether to transition from SaaS smokestacks to modular AI — the $285 billion market reaction suggests that question is settled. The question is how — and with what platform at the center.

The question for investors is which layer of the emerging stack captures the most durable value. The Clockspeed framework is clear: during every modular phase, the players that control the interfaces between layers — the orchestrators — extract a disproportionate share of industry profits. Intel and Microsoft proved this in hardware. The agentic orchestration layer is the equivalent position in enterprise AI.

The helix has turned. The disintegration phase is underway. AnyQuest is the orchestration platform built for exactly this moment.